Dry bulk holds firm; tankers correct moderately; clean and gas markets stay stable.

Smart ShipBroking’s latest Freight Market Outlook expands across four major shipping sectors, Dry Bulk, Dirty Petroleum Products (DPP), Clean Petroleum Products (CPP), and Gas Carriers (LNG/LPG).

The bulletin tracks 20 benchmark routes powered by Soshianest AI models, offering 2–3-week projections with live “Forecast vs Actual” analytics available on the Soshia Connect Dashboard.

🔹 Dry Bulk Market

The Dry Bulk complex remains firm to steady, maintaining its late-October strength.

- Handysize (Continent–USEC) stable near $15 000/day, signalling consolidation after prior gains.

- Panamax Transpacific R/V lifted to $16 200/day, with owners holding leverage but models suggest mild cooling.

- Panamax Average Trip around $16 000/day, firm and range-bound.

- BSI 58 (Supramax average) rose to $15 100/day, sustained by ECSA–Singapore demand.

- Kamsarmax 1-yr TC Atlantic steady at $17 000/day, while Pacific holds near $15 700/day, both showing limited volatility.

Short-term bias: Balanced to firm with minor softening expected into early December.

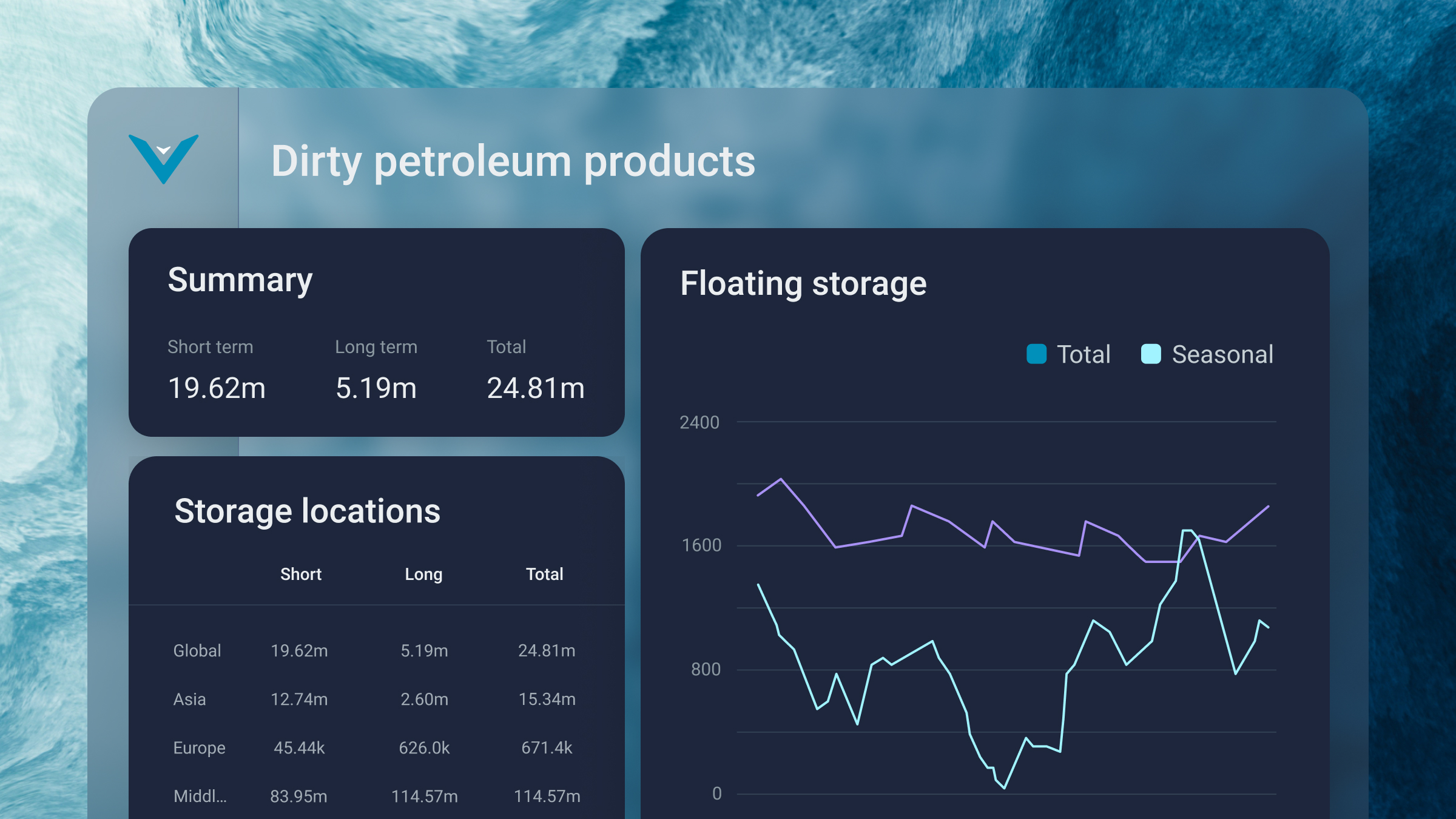

🔹 Dirty Petroleum Products (DPP)

The Crude and Dirty Product Tanker segment shows gradual correction after October’s highs but remains historically strong.

- TD15 (W Africa–China) eased to WS 108 (soft/corrective).

- Ras Tanura–LOOP firmed at WS 75, yet near-term moderation likely.

- Basra–Fos (Suezmax) steady at WS 115, stable but easing.

- Bonny–Rotterdam (Suezmax) holding WS 160, still elevated but due for correction.

- TD20 (W Africa–Cont) WS 158, soft/corrective.

- Basra–Fos TCE around $59 500/day, mild softening phase.

- Ras Tanura–Singapore (Aframax) WS 206, showing a controlled downward adjustment.

- Aframax Average TCE eased to $65 000/day, down from $67 000/day.

Overall tone: Corrective but not weak — still owner-weighted across key corridors.

Related : BIMCO: Crude tanker order book reaches nine-year high

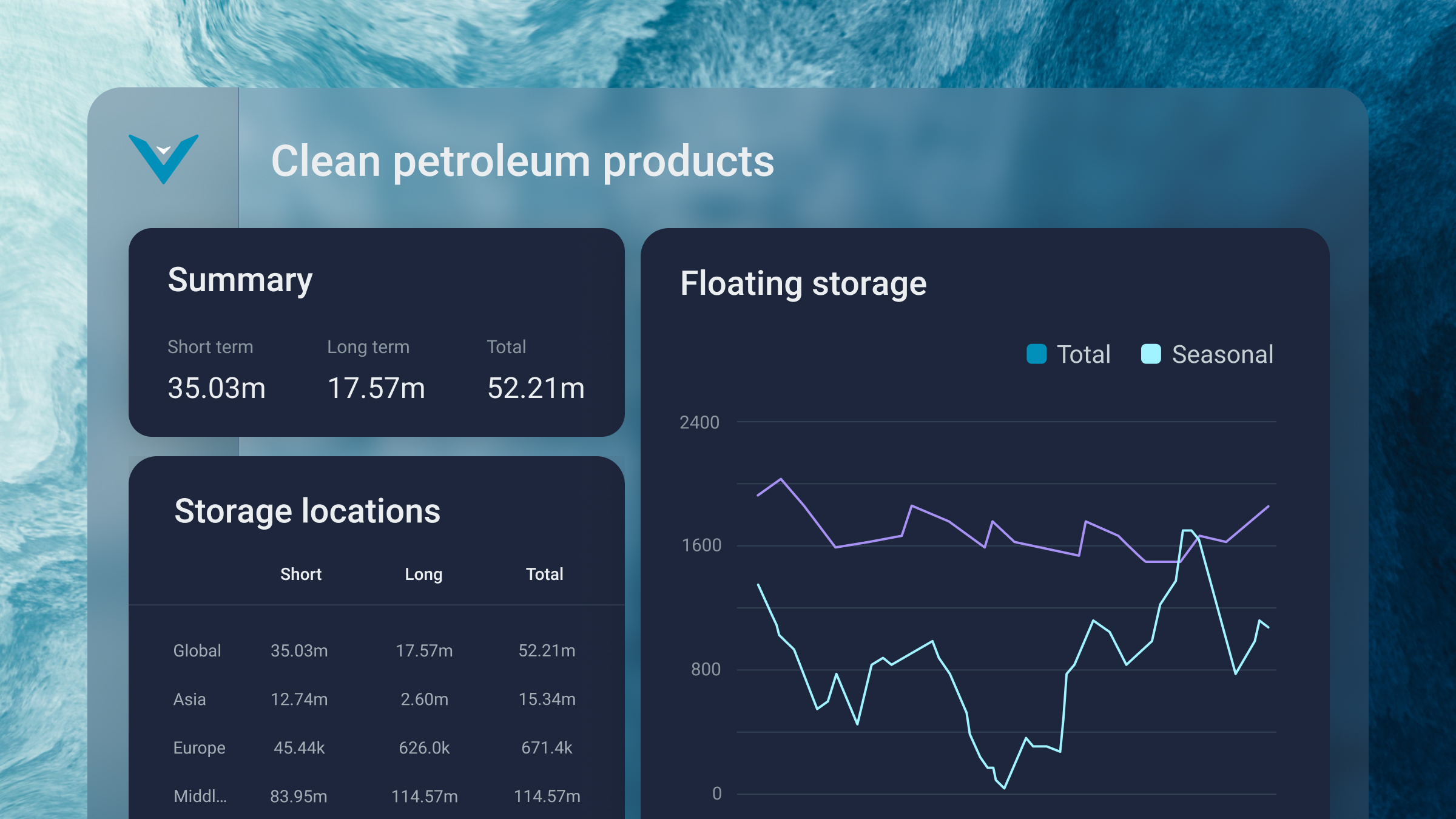

🔹 Clean Petroleum Products (CPP)

Clean product flows stabilised after strong Q4 movements.

- Ras Tanura–Chiba (35 k) steady at WS 150, balanced chartering.

- Mina al Ahmadi–Rotterdam (90 k) firm near $4.10 m, mild upside risk.

- Rotterdam–Chiba (80 k) $3.55 m, maintaining gradual firming.

Outlook: Steady to slightly firm through late November, supported by stable Atlantic-to-Asia trades.

🔹 Gas Carriers (LNG & LPG)

Gas segments remain flat-to-steady, reflecting equilibrium in charterer–owner expectations.

- LNG 145 k 1-yr TC around $8 800/day, within the $8.5–8.6 k range.

- VLGC 84 k 1-yr TC $42 000/day, neutral with mild soft drift.

- LPG 59 k 1-yr TC $32 900/day, correcting slightly from $33 700/day, entering a balanced phase.

Short-term tone: Flat, stable, and within historically elevated bands.

Across sectors, the Soshianest AI model suggests that while the post-October highs are moderating, most markets retain constructive balance. Dry bulk holds firm; tankers correct moderately; clean and gas markets stay stable.

Source : Press - Released received by Maritime Tickers

Freight Market Outlook , Week 47 , 17 November 2025 , Dirty Petroleum Products (DPP) , Dry bulk ,Clean Petroleum Products (CPP) ,Gas Carriers (LNG/LPG).Smart ShipBroking

You Might Also Like

22 December 2025

10 October 2025

Recommendation News

Marine Tech

Fincantieri :Agreement for two new cruise ships for Marella Cruises 10 October 2025

Shipping Lines

Rabie : Positive indicators suggest a recovery in canal traffic in the coming period. 21 January 2026

Incidents

Tragedy of the oil tanker "MERSIN" carrying 30,000 tons of fuel is being investigated 01 December 2025

Marine Tech

Container ship demolitions at an all-time low stands at 28 years 15 October 2025